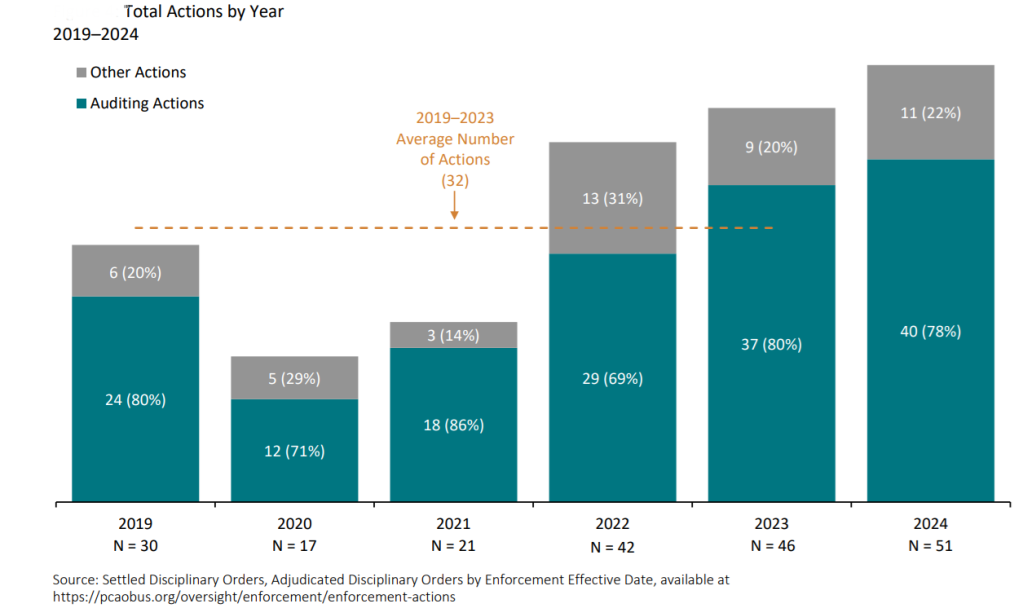

Total monetary penalties levied by the Public Company Accounting Oversight Board set a new record for the third consecutive year in 2024 as the number of enforcement actions reached levels not seen since 2017, according to a new report released on Feb. 26 by Cornerstone Research.

But with Paul Atkins likely taking over as chairman of the Securities and Exchange Commission, which oversees the PCAOB, a softer regulatory touch with accounting firms and a slowdown in enforcement activity could be forthcoming. Atkins, a former Republican member of the SEC during the George W. Bush administration, was picked by President Donald Trump to lead the SEC following the resignation of Gary Gensler last month. However, the Senate has yet to schedule confirmation hearings for Atkins. If/when Atkins is confirmed, he will likely fall in line with the Trump administration’s plans to dial back regulations and shrink government agencies, which could impact the future of the PCAOB. There’s a possibility that the PCAOB—which isn’t a federal agency but an independent entity—could be folded into the SEC or be eliminated entirely.

PCAOB enforcement during Trump’s first term as president wasn’t as harsh as it was during the four years Joe Biden was in office, which portends a downturn in activity while Trump is back in the White House. According to the Cornerstone Research report, PCAOB Enforcement Activity—2024 Year in Review, the PCAOB finalized 160 total enforcement actions, including 124 actions involving the performance of an audit, during Biden’s time as president. During the first Trump administration, the PCAOB finalized 126 total enforcement actions and 101 auditing actions. Total monetary penalties imposed were nearly seven times higher during the Biden administration, reaching approximately $68 million compared to a little more than $10 million during the first Trump administration.

“The type of respondents in enforcement actions shifted from a majority of individual respondents during the Trump administration to a near even split between individual and firm respondents during the Biden administration,” Russell Molter, a principal at Cornerstone Research and report co-author, said in a statement. “Additionally, the percentage of respondents fined in auditing actions climbed from a little over half (59%) to nearly all respondents (94%).”

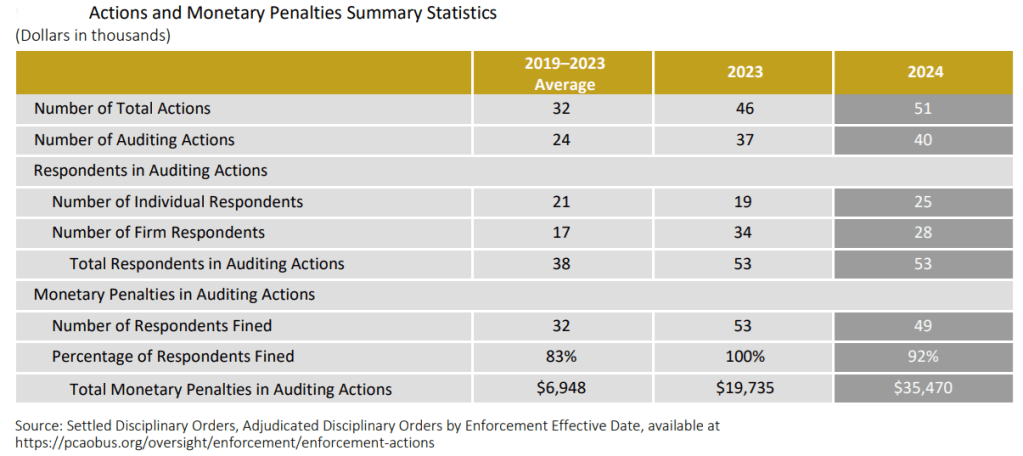

The PCAOB really ratcheted up enforcement during Biden’s last year in the White House, as the audit regulator publicly disclosed 51 total enforcement actions, including 40 actions involving the performance of an audit, in 2024—up from 46 total enforcement actions in 2023 and 42 in 2022.

Most of these enforcement actions came in the first half of 2024, with only 10 auditing actions finalized after the U.S. Supreme Court ruled against the use of administrative law judges in SEC v. Jarkesy.

At $35.7 million, total monetary penalties in 2024 marked a 78% increase over 2023. Since its inception in 2004, PCAOB enforcement has resulted in $94 million in total monetary penalties, 38% of which were imposed in 2024. In the last 20 years, the PCAOB finalized 487 total actions involving 675 respondents, the majority of which (344) were individuals.

“The PCAOB continued aggressive enforcement in 2024, finalizing 30 auditing actions in the first half of 2024, more than triple the number of actions finalized in the first half of 2023,” said Jean-Philippe Poissant, a report co-author and co-head of Cornerstone Research’s accounting practice. “In one in five auditing actions, the PCAOB alleged violations of not only auditing standards but quality control standards and ethics and independence, as well.”

The blockbuster fine of 2024 was the $25 million penalty the PCAOB gave KPMG in the Netherlands last April for systemic internal exam cheating over a five-year period. It’s the largest fine the PCAOB has ever doled out.

The PCAOB found that widespread improper answer sharing occurred in the firm’s internal training program and that KPMG Netherlands lied to the PCAOB about its knowledge of the rampant cheating.

The firm’s former head of assurance, Marc Hogeboom, received a permanent bar and a $150,000 fine from the PCAOB.

“The growth and breadth of exam cheating in this case was enabled by the firm’s failure to take appropriate steps to monitor, investigate, and identify the potential misconduct,” PCAOB Chair Erica Williams said in a speech at the Ninth Annual Baruch Auditing Conference in December 2024. “The PCAOB does not and will not tolerate unethical behavior—or any other behaviors that erode trust and threaten the investor confidence our system relies on. The cases we investigate and ultimately decide to enforce involve complex and serious matters: from audit failures in cases involving financial statement fraud to taking on client work that firms can’t complete to altering workpapers to not performing sufficient work before signing audit opinions—the list goes on.”

The PCAOB also nailed Big Four accounting firm PwC US with a $2.75 million fine last March for quality control violations related to auditor independence.

PwC’s quality control policies and procedures were found to be deficient because “they didn’t provide reasonable assurance that the firm’s personnel would timely consult with qualified individuals or refer to authoritative literature or other sources when dealing with certain complex, unusual, or unfamiliar independence issues,” the PCAOB said in the disciplinary order for PwC.

Other key findings from the report include:

- The number of auditing actions involving U.S. respondents grew in 2024, but those involving non-U.S. respondents didn’t.

- For the first year since 2021, there were auditing actions in 2024 that referred to a company’s disclosure of a material weakness in internal control.

- In over half of the 2024 auditing actions (52%), the PCAOB alleged violations of quality control standards.

- 11% of firm respondents in 2024 auditing actions were required to retain an independent consultant, down from 15% in 2023.

“All of these actions not only put audit quality in question, these actions put investors at risk,” Williams said at the Baruch Auditing Conference in December. “Which is why, after examining the facts and circumstances of every case, this board has revoked firms’ registrations, barred individuals, required functional changes to a firm’s supervisory structure, required firms to retain an independent monitor to drive improvements and best protect investors, and issued fines—including more than $35 million this year. All of the actions taken by this board send the message loud and clear: If you put investors at risk, you will be held accountable.”

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs

Tags: Accounting, Auditing, PCAOB, PCAOB enforcement