Startup companies progress through various stages of raising outside capital as they grow. This often starts with seed funding from founders and/or angel investors, progresses into various rounds of equity financing rounds from venture capital and/or private equity, and often ultimately leads to an initial public offering (IPO). As companies journey through this financing life cycle, it’s common for them to utilize bridge loans at some point to “bridge” liquidity needs in between financing rounds.

Many bridge loans deliver a host of complex accounting issues that commonly get overlooked. As companies go through the IPO process, they’re often required to revisit their accounting of these financial instruments.

In this article, I’ll highlight some of the common bridge loan terms that give rise to accounting complexities.

Common Bridge Loan Structure

Bridge loans typically have short-term maturities of one year or less. Since bridge loans are provided when a company is at risk of meeting its liquidity requirements, they carry substantial default risk. As a result, investors often require a higher investment return for their exposure to this credit risk.

Companies seeking financing through bridge loans often don’t have an appetite nor the ability to pay a high-interest rate on their debt as liquidity. As a result, these loans offer other rights and privileges to the investors to incentivize them to invest.

Variable-Share Settlement

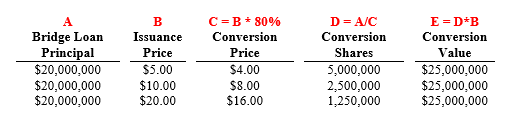

Bridge loans are often offered to investors who are expected to participate in the next round of equity financing. As such, it’s common for bridge loans to permit or require the issuer to settle its obligation by delivering a variable number of its shares (i.e., variable-share settlement). This allows the bridge loan to effectively serve as an advance on future equity financing.

The loan agreement often describes this feature as a conversion option; however, due to the variable-share settlement based on a fixed amount, this feature doesn’t expose the holder to any equity risk of the issuer upon settlement. For example, the conversion option may state the following:

Upon the closing of the Next Qualified Financing Event, the principal plus all accrued interest of the bridge loan automatically converts into the equity securities offered in the Next Qualified Financing Event at a conversion price equal to 80

Fixed-Share Conversion

Additionally, bridge loans often contain other features that protect the investor in the event the issuer is unable to close their “Next Qualified Financing Event”. One common feature is a true conversion option.

True conversion options typically provide the lender with an option to convert the bridge loan into a class of shares that existed when the bridge loan was issued. The conversion price is often fixed at the issuance price of the most recent equity round or the fair value of those shares when the bridge loan is issued. Because the price is fixed, it exposes the lender to the fair value of the underlying shares.

Accounting Considerations

Due to the complexity of the accounting literature that governs these instruments, it’s common for some accounting issues to be overlooked. Below are some items issuers should carefully consider when determining the appropriate accounting for bridge loans.

ASC 480 Considerations

Because the legal form of a bridge loan is debt, it would be recognized as a liability. However, because these instruments often contain variable-share settlements for a fixed monetary amount, the issuer must consider whether the bridge loan is within the scope of ASC 480.

The bridge loan will be within the scope of ASC 480 if it (1) obligates the borrower (either conditionally or unconditionally) to issue a variable number of shares equal to a fixed monetary amount and (2) this obligation is the predominant settlement outcome at inception.

Careful consideration should be given when evaluating whether the bridge loan meets both criteria above, as appropriate accounting classification can change based on the specific terms included in the agreement.

Embedded Derivative Considerations

If the bridge loan isn’t subsequently measured at fair value (either under ASC 480 or through the fair value election under ASC 825), any embedded derivative features should be evaluated for bifurcation under ASC 815-15.

Although variable-share settlement features are often described as “conversion” features in the loan documents, they generally don’t expose the lender to changes in the fair value of the company’s shares. Therefore, they should be evaluated as redemption features, not conversion features. If a discount is offered to the conversion price greater than 10%, there’s often a substantial premium that triggers derivative accounting.

A true conversion option must also be assessed; however, these generally aren’t required to be accounted for as embedded derivatives as they are gross settled in private company shares, which aren’t readily convertible to cash.

Beneficial Conversion Considerations

Additionally, if the issuer hasn’t adopted ASU 2020-06, they must consider whether the conversion feature is to be separated under the beneficial conversion feature model. To learn more about ASU 2020-06, check out the article, titled “Why Consider Early Adoption of ASU 2020-06?”

Effective Interest Considerations

As noted earlier, bridge loans often have a lower contractual interest rate where the investor is compensated with the discounted conversion price. Take the example above, where the investor effectively received a 20% discount to the next equity round. If the bridge load paid a coupon interest rate of 5%, and the expected term was one year, the yield would effectively be 25% (5% accrued interest and 20% through the discounted conversion).

ASC 835-30 describes the total amount of interest during the entire period of a cash loan to be measured as the difference between the actual amount of cash received by the borrower and the total amount agreed to be repaid to the lender. For that reason, it may be appropriate to accrete the redemption amount using the interest method, unless the fair value option is elected.

To further complicate this analysis, the accounting under ASC 480, 815-15, and 835-30 overlap. Careful consideration should be made to not double-count earnings impact.

=======

As Managing Director at Opportune LLP, Matt Smith assists companies with their accounting for complex financial instruments under both U.S. GAAP and IFRS. With over 15 years of client service experience at Opportune and Ernst & Young, Matt has gained extensive knowledge and expertise in debt and equity financing activities, derivatives and hedging, share-based payments, and SEC reporting. He holds an undergraduate degree in Accounting from Oral Roberts University and is a CPA licensed in the State of Oklahoma.

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs